基本情况

引入

1987年10月20号的纽约日报,从下图的标题可以看到“跌了508点,单日跌幅22.6%,交易量基本上翻倍”,“1987年和1929年是不是一样的?”等词,可以看到87年的股灾确实是很严重。

站在美国的角度,美国历史上有四次比较大的股灾。

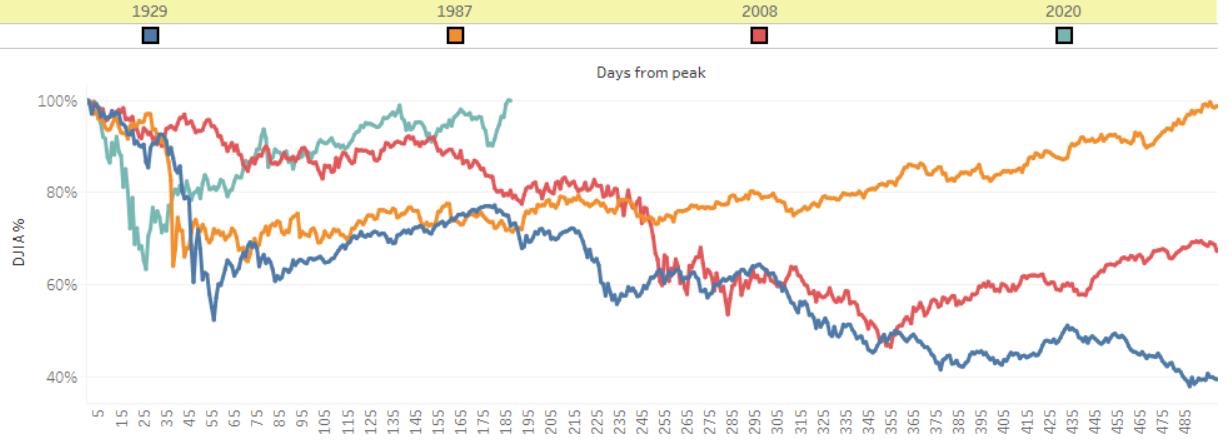

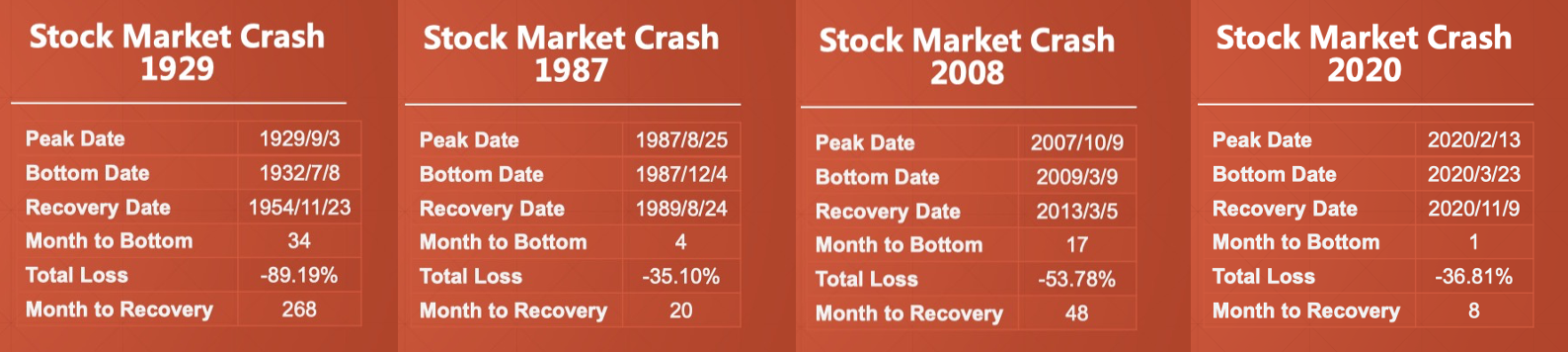

从下图的对比可以看到者四次股灾的时间、触底时间、跌幅、恢复时间。总的而言,1929年的股灾跌幅比较厉害,几乎3年才触底,而且一直用了22年才恢复,相比而言,2020年的股灾由于疫情跌的很快,但反弹恢复也是最快的。

技术背景

Portfolio Insurance 投资组合保险

- Portfolio insurance is the strategy of hedging a portfolio of stocks against market.(顾名思义就是给股票买保险,通过花出一点钱之后,希望整个投资组合的价值不会低过某个值)

- This technique, developed by Mark Rubinstein and Hayne Leland in 1976, aims to limit the losses a portfolio might experience as stocks decline in price without that portfolio’s manager having to sell off those stocks.(从下图可以看出这是一个非常标准的期权走势)

- 需要注意的是,站在1976年的角度看,由于(1)计算机能力有限(2)期权定价模型还没有完全出来,在这个前提下,这个技术当时是非常新的。

- Three methods to insurance the portfolio(共同特点就是追涨杀跌)

- Long stocks and bonds, and Long put options

- Long risk-free bonds and Long stock call options

- Dynamic Asset Allocation Strategies between stocks and bonds

- –> Buy more stocks when market keeps rising, sell more stocks when market keeps falling.(没有期权的时候,就自己动态创造一个期权出来)

- Costs: option costs and trading costs

- Price imbalance caused by strategy stampede(这是整个交易中间最大的问题,会产生一些价格不平衡要点)

Index Arbitrage 股指套利

- Designed to produce profits by exploiting discrepancies between the value of stocks in an index and the value of the stock-index futures contracts.

- 即在期权和现货中间找差价,买便宜的,卖贵的,因为在结算日的时候,期货和现货的价格会趋于一致,这样就赚到了中间差价。

DOT System

- Order processing system (纽交所的交易基本都是靠专家撮合为主)

- Allowed NYSE member firms to

- transmit large volumes of buy and sell orders through their own connections to the NYSE common message switch(会员公司的单子可以通过交易通道传输到纽交所)

- have them routed to a specialist/trading post(这些单子会路由到专家或者进行tarding post)

事件过程

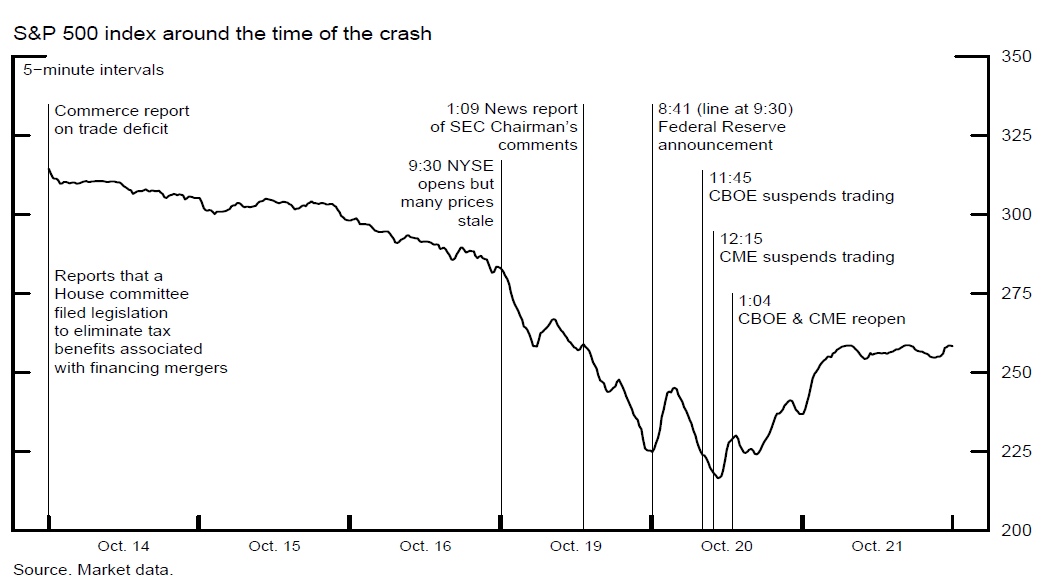

Oct 14

- 从宏观角度而言,在14号的额时候,有一些交易报告就出来了,说金融机构在并购中间的一些税收优惠可能没有了。

- 即在14号的时候,市场就传出了对整个市场走势不利的宏观因素。

Oct 16 (FRI)

- A variety of stock index options expired on Friday;(从微观角度分析,16号是周五,传统上周五是期权的到期日,有很多期权在这一天到期。)

- Investors could not easily roll their positions into new contracts.(但这天有很多投资者发现找不到合适的期权去延期。延期意思是仍然保持原有的position,方法是使用一个新的期权合约去替代已经到期的期权合约。(但道理上不应该在期权到期的最后一天才去延期,应该提前的))

- Investors went into the futures markets to sell futures.(这个时候没办法买卖期权,投资者就只能直接去卖期货)

- Increased sales of futures contracts(导致了期货卖得很厉害)

- created a price discrepancy between the price of the index futures and that of the stocks.(期货卖的太快就导致期货价格和股票的价格之间产生了价差)

- Index arbitrage traders took advantage of this price discrepancy to buy futures and sell stocks, which transmitted the downward pressures to the NYSE.(指数期货套利的人就发现了,卖期货的人很多,虽然价格还没传到股票这边,但是他们觉得期货的价格太低了,股票的价格太高了,所以追涨杀跌,也就是把期货买进来,然后把股票卖掉。)(注意股票交易在纽交所,期货交易在CME等)

Oct 19 (Mon)

- Large imbalance in the number of sell orders relative to buy orders at the opening of stock market(周一股市开盘的时候,新信息已经进入市场了,买卖出现了巨大的不平衡。整个股票交易所,卖单数量太大,买单数量太少。因此产生不了开盘价,因此价格还是周五收盘的价格。)

- Futures market opened on time with heavy selling(期货交易所这边期货的价格更低了,卖压非常大)

- Index-arbitragers sell stock at market price and long futures(既然价格还是周五的价格,套利者仍然是卖股票买期货的策略)

- Portfolio insurance(这个时候Portfolio insurance也自动触发了信息,股票价格越低,就要卖股票,加剧了股票的卖压)

- 所以整个市场19号的时候跌的更快了,很多人已经在担心股市会不会暂时关门了,这个时候有负责人出来讲话了,说了一段模糊不清的话,暗示交易所可能会关门。他虽然是想避重就轻,觉得可能会关门,但是这种模糊的信息传递到下面,大家就会觉得必然要关门了,事情就进一步发酵了。

- “There is some point, and I don’t know what point that is, that I would be interested in talking to the New York Stock Exchange about a temporary, very temporary, halt in trading”

Oct 20 (Tue)

- The NYSE moved to prevent index arbitrage program traders from using the DOT system to execute trades, which may have affected the depth of the market.(到20号的时候,纽交所发现很多股票的卖单处理不完了,因此禁止指数套利的这些人使用DOT系统。–> 这其实是不好的,因为市场下跌的时候如果没有这些套利者,市场的流动性会更差)

- Margin calls(期货市场这边也由于跌的厉害,margin call来了,需要进行保证金补仓)

- 所以20号这天,CBOE和CME都是短暂进行交易,进行紧急磋商,筹集到资金之后才敢重新开放,但是那一天已经跌的非常厉害了。

启示

- Impact of margin calls on market liquidity and market operation (margin call对整个市场的流动性影响非常大,之后才开始重视)

- Role of program trading strategies (program trading的策略在中间也起到了推动作用,现在Portfolio Insurance已经不太流行了,因为发现在跌市的时候根本起不到保险作用,保险公司还是要破产 )

- Difficulty to obtain reliable information.(信息的重要性,因为股票的信息更新非常慢,期货的信息更新相对快的时候,如果整个市场的信息透明度提高,能够无差别地传给所有的市场参与者,那么可能就不会引起恐慌,加剧市场的风险点)

- 虽说后面美国市场仍然有一些高频交易引起的闪崩,但是每一次股灾还是能够解决不少当时的市场问题。